Summary

- The CEO tells TheStreetSweeper that INUV board is considering a stock offering now that the stock price is high.

- The internet company’s lifeblood – website traffic – has shown a striking decline for INUV’s key properties.

- Net revenue fell in 2014; and the current share price of ~$3 already exceeds the sole price target of $2.

- INUV’s price-to-earnings is about three to five times higher than its peers, while its EBITDA is a fraction of the EBITDA of PERI and BCOR.

- INUV’s cash balance low compared to debt. Along with weak institutional ownership, this is yet another reason a stock offering makes sense.

By Sonya Colberg, TheStreetSweeper Senior Editor

Arkansas-based Inuvo (NYSEMKT:INUV) is working in a business that elicits the same level of enthusiasm as, say, receiving a dinnertime call from a telemarketer or getting a visit from a solicitor peddling a coat-full of fake Rolex watches.

INUV and its peers have seen a lot of doors slammed on their businesses previously. And this internet marketing and technology company could see more slammed doors in the near future.

Let’s look at INUV’s background and then get right to the top reasons TheStreetSweeper is watching for a decline in INUV’s stock – likely below the $2 level.

Investors should also take a look at other viewpoints on INUV here.

Background

Recent hype that Google (NASDAQ:GOOG) (NASDAQ:GOOGL) and Yahoo (NASDAQ:YHOO)have renewed deals with INUV are actually quite routine. Virtually all companies in this space have a relationship with the two websites, though these relationships seem to change rather often.

A big change occurred a few years ago in the toolbar business that was making millions for INUV and others. The Internet version of the solicitor banging on the door at dinnertime, these toolbars automatically installed when you downloaded a video. A search in the toolbar would be an INUV search, powered by Yahoo or Google. And the revenues from ad clicks were shared by the toolbar vendor and the search company.

But Google made a small change that drastically dropped toolbar downloads. Bye-bye searches with random Kim Kardashian rear-end pix popping up. Bye-bye key market opportunity for INUV and peers.

So INUV transitioned out of toolbar downloads. The company now focuses on the digital publishing business and building ads for other web publishers.

CEO Richard Howe told TheStreetSweeper that INUV works at keeping fresh, interesting content in its properties focusing on health, finance, careers, travel and local interests.

“On the ad tech side, the key there is really to build new and better ad units,” he said. “These would be ads that you see on the website when you go visit the website. You may think they’re ads that just sit there and don’t do anything, but the ones that perform the best have some sort of intelligence behind them.”

A long-time analyst in this space offered a less romantic perspective.

“At the end of the day,” he said, “these are banner ads.”

It’s such a fast-moving space that it even sometimes gets ahead of INUV. In one slightly awkward moment during the interview, we wondered about the “TastyNewDishes.com” that INUV promoted in its February corporate presentation, on page 8, here. We couldn’t find it in our internet search.

“Sometimes publishers leave, right? So we may … need to revise the presentation,” said Mr. Howe, noting someone else mentioned the same thing this week. “I’ve got to go look into why.”

Stock offering? CEO says, “It’s certainly something that our board is now talking about.”

Mr. Howe told TheStreetSweeper that a stock offering has not been “something we have contemplated up until now.”

He said the board hadn’t considered a raise before because they didn’t want to cause dilution since it wasn’t necessary.

“It’s not like we need the money,” he added.

“Now that the stock price is rising, while we haven’t decided to do an equity raise, it’s certainly something that our board is now talking about,” said Mr. Howe.

He wouldn’t elaborate on exactly how soon a stock offering might happen.

“Whether that means we’ll do it or not, is a whole other story. And, like I said, we’re certainly not in any hurry to do it,” added Mr. Howe.

Striking decline in INUV’s website traffic

The number of unique visitors, so vital to growth for companies like INUV, has shown a stunning decline of about 50 percent for INUV over a year. See the chart below, measuring the traffic to INUV’s http://health.alot.com/website, according to the “Nielsen of website traffic,” Compete.com:

Source: Compete.com

ALOT, www.alot.com, is one of INUV’s primary owned and operated properties. But its chart, too, shows the unique visitors number is significantly declining.

Source: Compete.com

These charts clearly show, in our opinion, a dying Internet business.

*If business is so good, why are net revenues declining?

Look what has happened since Google’s policy change. Net revenue has declined 10 percent year over year:

(click to enlarge)

Gross profit grew slightly primarily because INUV cut some costs. But a company generally can’t cut its way into growing a business. However, INUV did see an encouraging jump to $15.5 million revenue in the fourth quarter, but INUV also just announced plans to move into a larger, more expensive building, which will add to expenses and undoubtedly distract management in the process.

Additionally, INUV is plagued by a history of losses, anyway, according to the company 10-K:

“We have a history of losses and there are no assurances that we can consistently generate net income. Although we generated net income in 2014 and 2013, we have a history of net losses that have resulted in an accumulated deficit of $119,088,552 as of December 31, 2014. We cannot provide assurance that we can consistently generate a net income”

At the same time, investors must keep in mind INUV’s history and the overall industry’s history. While Mr. Howe said the company works well with Yahoo and Google and has been able to adjust, company filings note that the business remains at constant risk of another advertisement policy change:

“… they will from time to time implement policy changes that impact our ability to display ads within our networks. Such changes may cause significant volatility in our revenue and earnings. The loss of either of these customers would have a material adverse effect on our business.”

Shares exceed the price target.

INUV shares are about $1 higher than the $2 price target set by the only firm that has set a price target. That was just in February, and we’ve seen no update.

(click to enlarge)

Weak institutional ownership

A strong company will attract strong institutional ownership. But investors can see that INUV has generally fallen short in this respect:

(Source: Yahoo Finance)

Cash balance is low, especially compared to debt.

At $3.7 million, INUV’s cash balance looks low to us. It looks even worse compared with the debt balance – which is $3.6 million.

According to the company’s 10-K:

“Failure to comply with the covenants and restrictions in our credit facility could result in the acceleration of a substantial portion of our debt, which we may not be able to repay or refinance on favorable terms. We have a credit facility with Bridge Bank, N.A. (“Bridge Bank”) under which we had approximately $3.6 million in debt outstanding as of December 31, 2014…”

“We have historically had difficulties meeting the financial covenants set forth in our credit agreement. Our lender has given us waivers in the past and reset our financial covenants several times. In the event of a breach of our covenants we cannot provide any assurance that our lender would provide a waiver or reset our covenants. A breach in our covenants could result in a default under the credit facility… our ability to conduct our business as it is currently conducted would be in jeopardy.”

The immediate point is this: This is another reason it makes sense to complete a capital raise now.

EBITDA expectations “May be a little high.”

Analysts may be a little too optimistic. Mr. Howe said trying to meet analysts’ projected EBITDA (earnings before interest, taxes, depreciation and amortization) of $5.3 million in 2015 certainly won’t be easy.

Take a look at the chart below:

(click to enlarge)

Source: Bloomberg

Mr. Howe said plans to rebalance stock-based compensation more toward cash this year changes the cash flow part of EBITDA.

“The cash flow part of the equation has components that sometimes analysts get wrong,” he told TheStreetSweeper. “So they may be a little high on the EBITDA number.”

INUV stock is not attractively priced

“We’ve always believed the company was undervalued relative to its peer group,” said Mr. Howe.

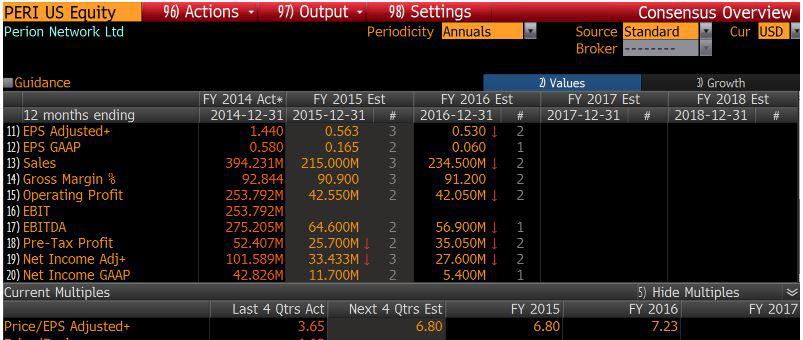

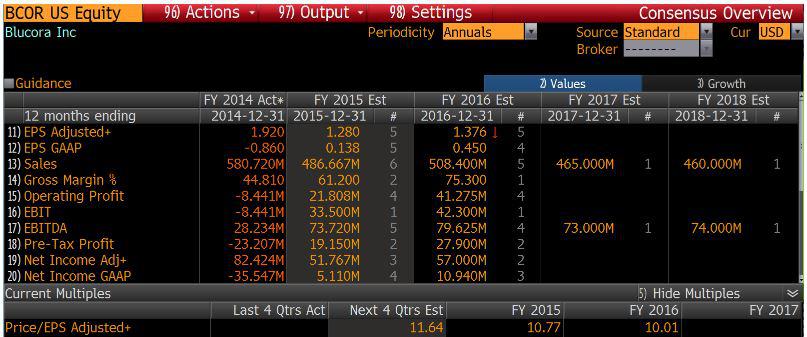

However, we disagree. Investors can see from the snapshots of charts below that, at about 37 times earnings, INUV is three to five times overvalued when compared with its rivals, Perion Network (NASDAQ:PERI) and Blucora (NASDAQ:BCOR). And look at INUV’s EBITDA of $4.2 million relative to PERI’s $275 million and BCOR’s $28 million.

(click to enlarge)

(click to enlarge)

(click to enlarge)

Shares are trading too high. Overall, the stock has had no good reason to rush to ~$3. But we believe there are many legitimate reasons for the shares to go screaming right back down to pre-rally levels.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Disclosure: The author is short INUV. (More…)The author wrote this article themselves, and it expresses their own opinions. The author is not receiving compensation for it. The author has no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: * Important Disclosure: The owners of TheStreetSweeper hold a short position in INUV and stand to profit on any future declines in the stock price. Editor’s Note: As a matter of policy, TheStreetSweeper prohibits members of its editorial team from taking financial positions in the companies that they cover. To contact Sonya Colberg, the author of this story, please send an email to scolberg@thestreetsweeper.org.